Johansen Cointegration

Description

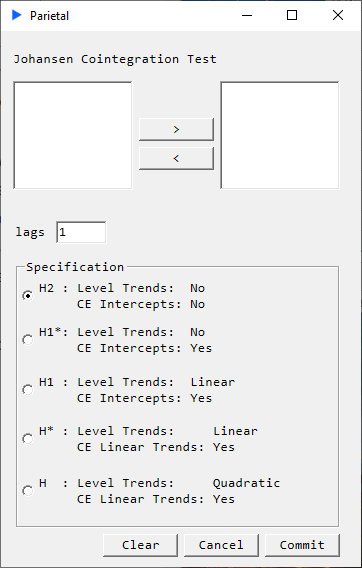

At its core, cointegration modeling allows us to capture long run dynamics by working with time series data in levels. The resulting model not only captures long run dynamics but the statistical properties (super-consistency) of the estimators themselves are superior to modeling time series data that is differenced. Johansen cointegration allows for certain specifications/restrictions on the VECM (i.e. H2, H1*, H1, H* and H) and takes Engle-Granger cointegration to higher dimensional data.

Note that as of v1.0.8 the Excel front-end outputs only the main test table. However, the engine returns further detailed metrics that can be parsed using the API.

Returns

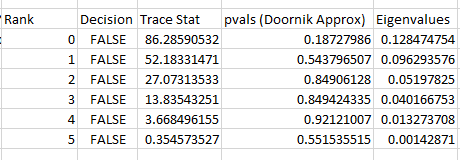

- Johansen table

- Cointegrating rank

- Decision

- Trace statistic

- p-values (Doornik Approximation)

- Eigenvalues