Generalized Linear Models

In cases where the dependent variable follows a distribution that is different from a normal distribution, we have a technique that generalizes OLS principles. This is known as the generalized linear model (GLM). If the target distribution falls under the *exponential family* of distributions, it uses a link function as a bridge to map the regression. Typically the method of iteratively reweighted least squares is used to fit the model due to quick convergence properties.

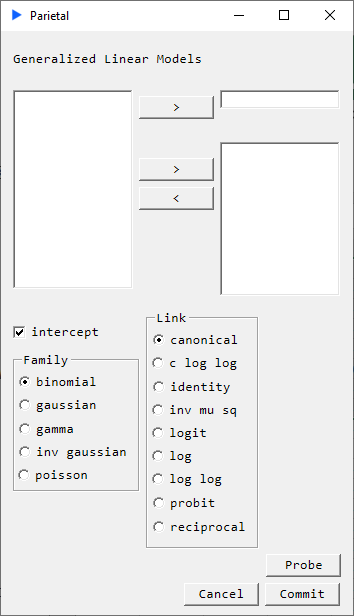

- Families

- Binomial

- Gaussian

- Gamma

- Inverse Gaussian

- Poisson

- Links

- Canonical

- C Log Log

- Identity

- Inverse MuSq

- Logit

- Log

- Log Log

- Probit

- Reciprocal

Description

For a GLM, three pieces are needed:

- A distribution belonging to the exponential family

- A linear predictor

- A link function that maps the linear predictor to the target distribution

The exponential family of distributions are ones whose density functions can be expressed in the form of:

$$ f_Y(\mathbf{y} \mid \boldsymbol\theta, \tau) = h(\mathbf{y},\tau) \exp \left(\frac{\mathbf{b}(\boldsymbol\theta)^{\rm T}\mathbf{T}(\mathbf{y}) - A(\boldsymbol\theta)} {d(\tau)} \right) $$

We implement the following families:

- Binomial

- Gaussian

- Gamma

- Inverse Gaussian

- Poisson

We describe the linear predictor as. $$ \eta = X \beta $$

Then we define a link function that maps this linear predictor to mean of the target distribution. $$ E(Y \mid X) = \mu = g^{-1}(\eta) $$

We implement the following links:

Canonical (will choose the default link for the chosen Family)

Family: Gaussian → Link: Identity

Family: Binomial → Link: Logit

Family: Poisson → Link: Log

Family: Gamma → Link: Reciprocal

Family: Inv Gaussian → Link: Inverse Mu Squared

C Log Log

Identity

Inverse Mu Squared

Logit

Log

LogLog

Probit

Reciprocal

Returns

- coefficient

- standard error

- t-statisitc

- p-value

- convergence

- fisher iterations

- residual null

- residual deviance